Investing – Staying The Course

I stumbled across an excerpt written by a highly respected investment professional. Take a look:

“There are many financial concepts we can apply metaphorically to our personal lives, like diversification (having varied interests), asset allocation (considering where we put our time and energy), and rebalancing (taking time to reflect and adjust).

But, while investing needs to be from the head — as logical, rational and unemotional as possible — our relationships with others and the world around us needs also to be from the heart — as sensate, vulnerable and empathic as possible. However, inevitably, in both cases, we will suffer loss.”

In life, we go through cycles of good, mediocre, and rough patches. Why should investing be any different? The disciplined and patient investors find opportunities, even optimism, during the worst of times.

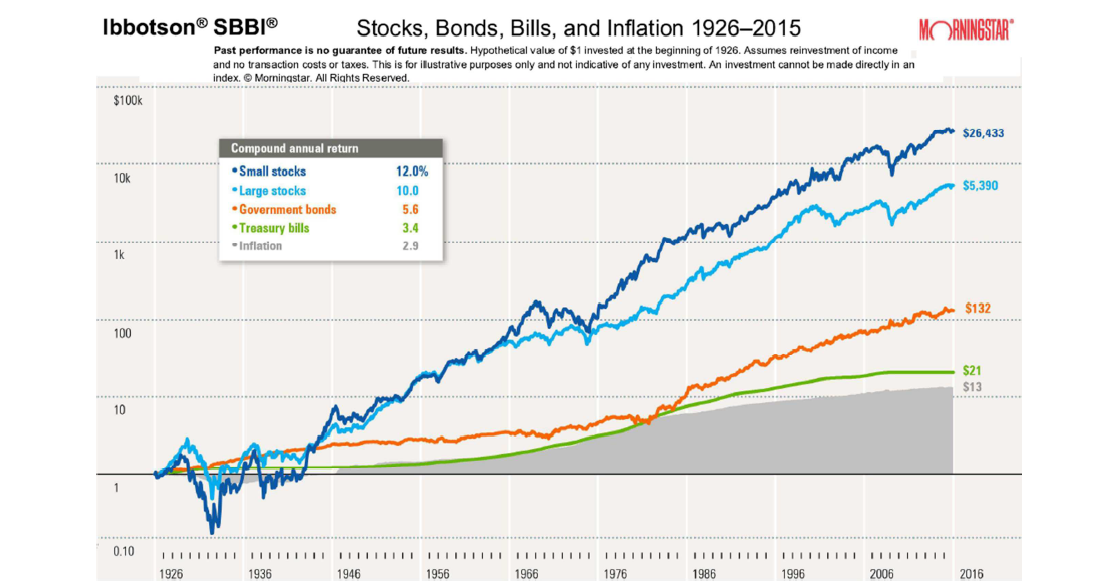

Over 15 year periods, history has shown us that U.S. stock markets are up 100% of the time. In the short term, stocks are less predictable. But, the growth of the global economy has been upward trending. But, inevitably, there will be market corrections. Some corrections may be small, some may be bigger. There will even be full blown stock market crashes on occasion. Review the following graph. This shows why stock market investing is key to adding wealth (rather than leaving the money in a checking or savings account). Stock market investing is what outpaces inflation and adds real wealth over the long term.

The issue with leaving all of one’s money in a checking/savings account is that the individual loses their buying power due to inflation. Treasury Bills and Government Bonds tend to keep up with inflation, but not much more than keep up.

Let’s talk about Compound Interest. If an investor’s goal is to save $5,000,000 (before taxes) by age 65, assuming a hypothetical 10% rate of return, the 25 year old (with a 40 year time horizon) has to put away $785 each month. That equates to a total of $376,800 of their own money, which means $4,623,000 (or 92%) of their wealth comes from compound interest. Let that sink in. Over 40 years (age 25 to 65), the investor puts in $376,800 and has a little more than $5,000,000.

However, the 45 year old wishing to accumulate the same $5,000,000 by age 65 (this time only having a 20 year time horizon) will need to save $6,500 per month to reach their goal. Again, this assumes a 10% return. The 45 year old will save $1,560,000 of their own money (over 3x as much as the 25 year old), which means $3,440,000 (or 68%) of their wealth comes from compound interest. Over 20 years (age 45 to 65), the investor puts in $1,560,000 and has a little under $5,000,000. Still not too shabby, but the individual who invests for a 40 year time horizon is much better off.

So why does the 45 year old have to shell out over 8x more each month? Because, the way compound interest works, the longer you remain invested, the more your army of dollar bills goes to work for you.

Look at the chart below. This shows $1,000 invested, nothing more, and compounded at a 10% rate of return for 20 years. The compound interest curve gets steeper the longer we remain the course. The army of dollar bills at work grows stronger and more abundant over time.

![]()

Article by Matt Ward