You have 4 options for inheriting your spouse’s IRA.

- Roll over the assets into a new or existing IRA in your own name.

- Transfer the assets to an inherited IRA.

- Roll over the IRA assets into a new or existing IRA and convert the assets to a Roth IRA.

- Disclaim (decline to inherit) all or part of the assets.

1. Roll over the assets into a new or existing IRA in your own name

As a surviving spouse, you have one option that nobody else has: rolling over inherited IRA assets into an IRA in your name and treating those assets as if they were your own. If you have not reached age 70½ but your spouse had, this option enables you to delay taking distributions until you reach age 70½, rather than continuing your spouse’s RMDs.

Keep in mind that if your spouse was age 70½ or older at the time of death, you will need to determine whether they met the RMD for the year in which they passed away. If your spouse did not meet the RMD, you must take an RMD for that calendar year by December 31.

2. Transfer the assets to an inherited IRA

Transferring assets to an inherited IRA may make the most sense if you are under age 59½ and need to access some or all of your spouse’s IRA assets now, or before you attain the age of 59½. Why? Because you won’t be subject to a 10% penalty when you take withdrawals from an inherited IRA prior to age 59½ as you would be if you were withdrawing assets from a non-inherited IRA you may own.

Spouse inheritors also have additional rules regarding the timing of RMDs for inherited IRAs. You can begin taking RMDs in the year after the year of death, or you can delay beginning RMDs until your spouse would have turned age 70½.

Another option is to invoke the 5-year rule. As long as your spouse was under age 70½ when they died, you have 5 years during which you can withdraw inherited assets from an inherited IRA at any time, in any amount, as long as all the assets are withdrawn by December 31 of the 5th year following your spouse’s death. However, keep in mind that these larger distributions could push you into a higher tax bracket.

If you inherit a Roth IRA and transfer the assets to an inherited Roth IRA, your RMDs will always be treated as if your spouse were under age 70½. Unlike Roth IRAs owned by the original owner, inherited Roth IRAs do require annual RMDs, and you must begin RMDs by December 31 of the year following your spouse’s death. These RMDs will be based on the Single Life Expectancy Table. Or you may elect to take distributions under the 5-year rule. Withdrawals from inherited Roth IRAs are normally tax-free as long as the original Roth IRA was funded for 5 years or more.

3. Roll over the IRA assets into a new or existing IRA and convert the assets to a Roth IRA

If you don’t anticipate needing to rely on RMDs from your spouse’s IRA to pay your living expenses, you may want to consider rolling over the assets into an IRA in your name (option 1, above) and then converting the assets into a Roth IRA. This assumes that the IRA you inherited is a traditional IRA and not already a Roth IRA.

With a Roth IRA, contributions are not tax deductible, but you pay no tax when you withdraw assets, provided certain conditions are met.

4. Disclaim (decline to inherit) all or part of the assets

If you choose this option, the IRA assets will pass to your spouse’s contingent beneficiaries. This could be your children or grandchildren, another relative, a trust, or a charity.

When assets pass directly to the IRA owner’s children or grandchildren, the potential for tax-deferred (or tax-free) growth will be stretched out over a much longer period. Though the children or grandchildren will need to begin taking RMDs in the year after the IRA owner’s death, RMD calculations will be based on the longer life expectancies of these younger inheritors.

In some cases, disclaiming IRA assets can be a smart estate-planning move, especially if your spouse’s estate was not structured properly. While assets you inherit from your spouse are generally not subject to estate taxes, they do become part of your estate when you die. Be sure to consult a tax professional or attorney.

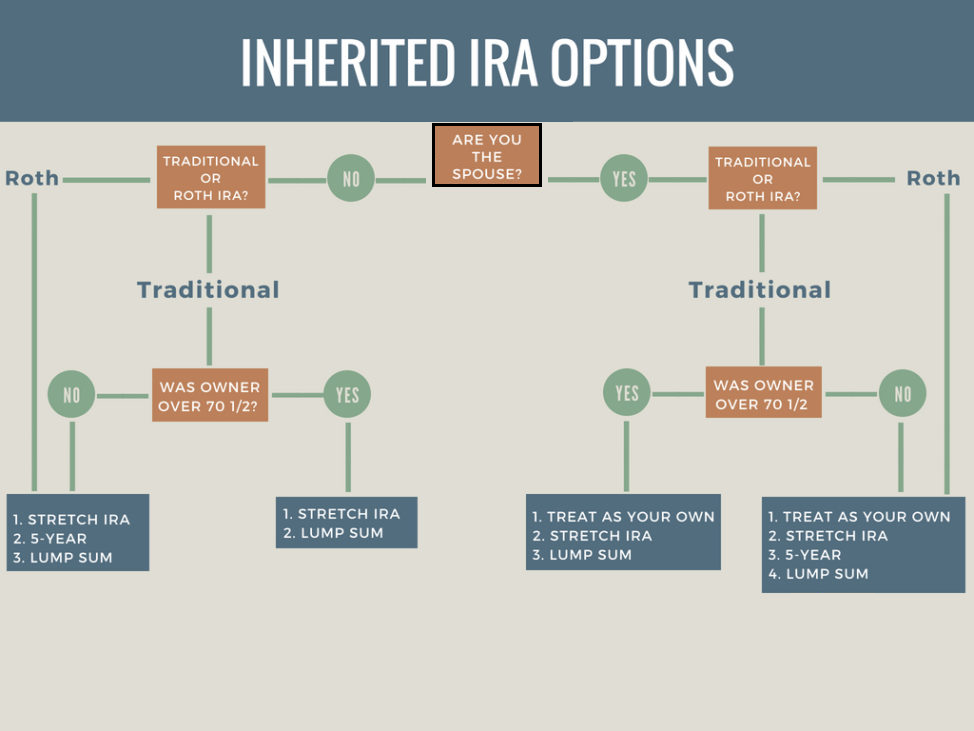

Here is a great article from Fidelity that explains the different options you have for inheriting your spouse’s IRA. See this chart below for a visual understanding of the rules around inherited IRAs.

Article summarized by Matt Ward

*This article was written prior to both the SECURE Act & 2.0 Act passing. Please contact us or your qualified advisor for information on your individual situation.